Weather Proof Investment Strategies

Weather Proof Investment Strategies

Through market crashes, financial crises, and economic slowdowns, you can follow some simple strategies to keep your portfolio from getting wiped out

By Doby Atilano

Every time the market undergoes a massive correction or when a crisis sprouts from any economy, investors are usually scared to start investing. We can see this through sales reports of most financial institutions during an economic crisis. In addition, investors are not just scared to reenter the market during the bad conditions; most have also lost a big portion of their investment portfolios so they will need as much cash to finance themselves during the difficult times. This leads many to have less disposable assets to invest in during the crisis.

However, this is not true for all investors. Those not focused on fund returns but on their investment strategy prevail even in tough times. Most of us have heard or learned through newspapers and investment gurus that “dollar cost averaging” is the best way to invest your money.

However, due to a lack of discipline or a swing of negative emotion, even investment gurus that teach the strategy or people that are well informed still deviate from it and incur massive losses especially during a crisis.

Usually, the reason is temptation to be over exposed during a flourishing market, which usually bites the investor’s back when the market turns sour the next day. A sharp and disciplined investor will first find out his risk appetite to determine how much risk he is willing to take and whether or not it is suitable for him to invest in equities, fixed income securities, treasuries, or a mixture. After which, he will be able to determine what proportion of his portfolio he should put in an asset class.

Diversification through time

Since most investment vehicles that provide significant returns swing up and down with greater volatility, one should only put a maximum of 10% of his monthly income in order to buy the same units or shares at different points in time – a method called “diversification through time” or “dollar cost averaging” (or in our case, peso cost averaging).

Some units will be purchased at an expensive price, which could lead to paper losses when the market dips, and some units will be purchased cheaply (in most cases during an economic crisis), which will compensate for the previous losses and magnify the returns during an inevitable rebound or an upswing in the market.

The key to be able to apply this method consistently even in hard times is to only expose a small amount of your earnings per month in a vehicle that moves up and down and to keep a considerable amount of liquidity. Some experienced investors only expose their interest income from their very liquid high yield deposit accounts. The more frequent and the longer an investor invests in one particular fund, the less risk he will have to take.

Financial history clearly shows that markets always end up higher in the long term. Furthermore, the risk is further reduced because of the investment frequency or diversification through time.

Generally, most investment products that provide substantial returns in the long term such as equities or stock move towards only that directions and that is upwards (when we are lucky), sideways, or downwards (which seems to occur more often these days). If we expose more than 10% of our savings in an investment tool that goes up and down, we will feel big losses and get affected if the market suddenly goes down.

In conclusion, investing during a downward trending market or even during a financial crisis makes sense if we apply “diversification through time” or “peso cost averaging” and if we only invest 10% or less from our monthly income.

We have also seen that investing more frequently into one particular investment that moves up and down can substantially reduce risk. Furthermore, risk can even be further reduced if the strategy is consistently followed during the long term. In essence applying peso cost averaging on a downward trending fund makes sense if done consistently and frequently over the long term as the unit prices of the chosen fund will be bought at very cheap prices, translating into magnified returns as soon as it recovers. Lastly, it also makes sense to brush off greed and not be tempted to get over exposed in volatile investments especially in a bull market as this can give significant losses when the market turns into a bear.

[Sidebar]

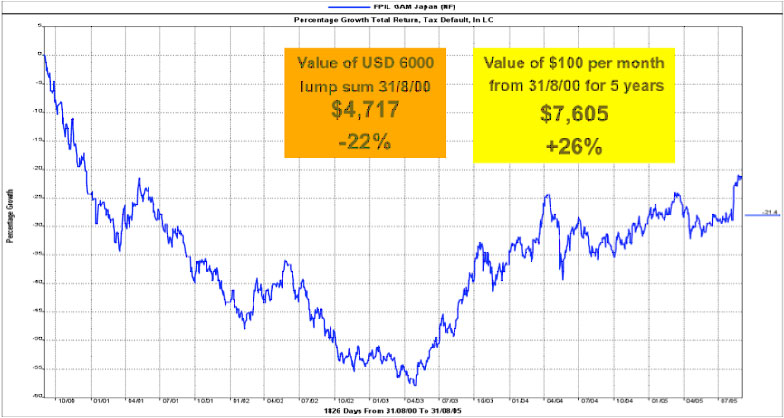

GAM JAPAN EQUITY FUND

GAM JAPAN EQUITY FUND

This example shows the performance of one particular fund after a big crash and a slight rebound that is still marginally lower than its crash. In this example, the fund did not get back to its previous high five years ago.

If you invested a one-time investment of $6,000 five years ago last August 31, 2000, five years after or on August 31, 2005, his money would have shrunk to $4,717. In this case if the $6,000 invested is more than 10% or more of your monthly income, you would have felt the losses and directly hit your current lifestyle.

However, if you took a dollar cost averaging strategy instead of looking at the fund’s return, and you invest less than 10% per month of your income, you would have either minimized your losses or earned substantially more than the investor who just put most of his money in the fund at one point in time.

Our example shows that if you invested the same amount of $6,000 over the same time period but in installments of $100 per month, you would not only have reduced your risk but also would have generated a substantial amount of return. In our example, you would have made a 26% return and increased your investment to $7,605. In this case, substantial downward swings from the fund has spared you from sacrificing your current and future lifestyle as you only exposed 10% of you income monthly or $100 a month. Small investments every month or year will not hurt you especially when there is a big downturn in the market.

[PULL QUOTE]

5 Weather-Proof Investing Strategies

Follow these simple strategies to whether any financial storm:

1. Apply diversification through time or peso cost averaging, investing every month a fixed number of units to capture different prices, including cheap ones especially during an economic crisis.

2. Invest 10% or less from your monthly income to minimize your exposure.

3. Invest more frequently into one particular investment that moves up and down, to maximize peso cost averaging.

4. Avoid the temptation to get over exposed in volatile investments and get caught in a market bubble about to pop.

5. Stay for the long haul, as financial history clearly shows that markets always end up higher in the long term.

[PROFILE]

Doby Atilano is a registered financial planner and founder of the Global Investors Center, a pioneering education facility specializing in global portfolio management. Bringing together representatives from Fortune 500’s top fund management companies abroad as trainers, this facility is keen on educating the general public in independently choosing the right investment opportunities abroad.

The seminars convened within the Global Investor’s Center will help impart proper investment knowledge to its students, giving them the opportunity to maximize their investment portfolios in a global scale. Lectures available include “Positioning Your Personal Finances for the Inevitable Market Rebound,” “Forex Trading: The Basics in Currency Trading,” “Investment 101 for Newlyweds: Building for Your Future,” “Benefits of Managed Futures in a Well Diversified Portfolio,” and “Save for the Longest Vacation of Your Life: Your Retirement.”

To learn more about the Global Investors Center, call tel. nos. 994-7424 or 328-8858, e-mail inquiry@gicphil.com, or visit their Web site at www.gicphil.com.