Saving for College

Saving for College

You’ve seen parents burned by education plans. But what’s the alternative? Here’s a college savings plan that won’t fold up

By Kendrick Chua

Norma (not her real name), who works for one of the biggest educational plan providers before, can’t help but cringe when asked how people are reacting now towards educational plans. Her facial expression mimics the sentiments of her clients, who have shown various ways of rejecting her.

Ten years ago, it was unthinkable that education plans will be met with such hostility. When educational plans were first launched some decades back, they were a much sought-after investment instrument by the public. After all, education is one of the major financial priorities of Filipino parents and the burden of a forthcoming college education cost is no laughing matter.

The pre-need educational plan was crafted precisely to address this concern of parents. The educational plan was a commitment by pre-need companies to pay their children’s tuition 16 or 17 years later in exchange for a minimum investment on the parents’ part. With an offer like that, who can refuse? Filipino parents’ dream of being able to send their children to the best colleges and universities was within easier reach. It became a huge success that other pre-need companies followed suit, thereby flooding the market with hundreds of thousands of education plans.

“I will often receive phone calls or beeper messages from people I never knew telling me they would like to buy an education plan. That was how lucrative selling education plans were.” The euphoria was widespread and the sales agents were having a heyday. Norma was a perfect example – she was able to build a house from the commissions she earned within several years.

Just when the exuberance seemed never to end, pre-need companies were suddenly confronted with soaring tuition when deregulation was introduced in 1992. The return on their investment just cannot keep up with the increase and this snowballed into the collapse of several pre-need companies in mid-2000 defaulting on their commitments to their plan holders.

Early this year, because of the collapse of the Legacy Group and later the sale of Pacific Plans to businessman Noel Oñate, the public eye once again fell on these pre-need companies and a Senate investigation ensued. What added oil to the fire was the admission from the Federation of Pre-need Plan Companies that their industry is suffering a dwindling trust fund as an effect of the global financial crisis. If not addressed soon, more pre-need companies may collapse and along with it, the dreams of thousands of Filipinos.

Crunching down the numbers

In the minds of everyone, education costs today are outrageous to say the least. Just ask any parents with kids currently in the tertiary level and you’d get the same response—a wide-eyed, open-mouthed sigh.

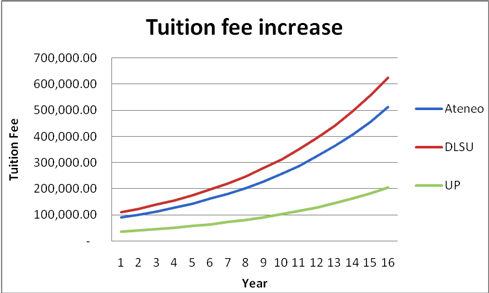

Sixteen years later, the figures are not going to look any less. According to the Commission on Higher Education (CHED), the average increase for college tuition is 12.25% per annum. That means, should you wish to send your child to either the top-tiered colleges like Ateneo de Manila, De La Salle University, or the University of the Philippines (see Table 1), be ready to churn out at least half a million pesos, multiply that by four years, and that would translate to a whopping P2,000,000!

Table 1: Sample College Tuition (in Php, as of March 31, 2009)

| Schools | TUITION SY 2008-2009 |

IN 4 YEARS SY 2012-2013 |

IN 10 YEARS SY 2018-2019 |

IN 16 YEARS SY 2024-2025 |

|

| Ateneo De Manila | 90,613.00 | 143,858.00 | 287,776.00 | 575,669.00 | |

| De La Salle University | 110,447.82 | 175,348.70 | 350,738.00 | 701,679.00 | |

| University of the Philippines | 36,000.00 | 57,141.00 | 114,332.00 | 228,709.00 | |

| Average | 502,019.00 |

What are the other ways to invest?

With the public trust on pre-need plans dwindling, it is natural for Filipino parents to look for other alternatives. After all, the need to send one’s child to college is still there, with or without the pre-need companies. Quality education is still perceived as the ticket to success by Filipinos.

Since prudent financial planning starts with a projection of the future cost of college, the problem comes in when investors put too much emphasis on the projection. Clients should be made aware that projections are just that—projections. “From point A to point B, nobody knows what will really happen and if those figures will still hold true,” says Alijeffty “Jeff” Gonzales, a Registered Financial Planner (RFP) and a consultant for business development for Insular Life and Assurance Company.

While the figures are there to serve as guide, it is by no means the end. If these multi-billion companies can hire the best actuarials in the land and still fail because of conservative estimates, how much protection does the ordinary Juan who invest on his own, has?

What can the ordinary person do then? “You can either invest on your own or purchase a plan,” Jeff says. While either or both of options are practical, there is one thing we should clearly remember, “Overinvest towards the goal,” he recommends, “Gone are the days when you have one product to match one objective. Now you need three or four to match one particular need.” In this case, it is better to have a surplus than to have a deficit.

Plan A: Investing on your own

For example, if you’re going to work towards having P2,000,000 after 16 years without the use of interest rates and yields, you need to save at the very least P130,000 every year to achieve the P2,000,000 mark 16 years later. Even with the use of a 4% interest rate, you need to still need to save P90,000 every year. Clearly, it is not an easy figure to save for salaried employees. Surely, there is a better way.

Gonzales cites that the recently issued corporate bonds offer very attractive coupon rates with some reaching as high as 9% interest per annum. The only problem with the bonds he added is that they mature after five years. “There would be no matching after then.” At the given rate, an initial investment of P500,000 pesos would be P1,900,000 after 16 years—maybe enough to fund the college education of your child. The challenge after the maturity is to look for an investment that offers the same yield.

Stocks are also another investment instrument one can consider but it entails greater risk. Since the start of the bull run in 2003 all the way to the 2007, stocks have been averaging a whopping 22% growth per annum. The same P500,000 invested now has grown to more than P1,600,000 in just five years! Sounds great but let’s go back further and imagine if you have invested in 1997 with the same objective, the same P500,000 12 years later is just valued at P260,000. That means your investment in those 12 years didn’t earn anything and has to earn more than a 100% just to recoup the losses and earn a little profit. Stocks may well be the best instrument to leverage against skyrocketing tuition hikes but wild volatility can really burn your hard-earned savings.

If you don’t have the resources to invest in either of the two, mutual funds may be another option, Hector de Leon, RFP and First Vice President of First Metro and Asset Management., points out, “A strategy you can employ is to use the gains from a conservative fund and reinvest that into a more aggressive one.”

Plan B: Purchasing a plan

Since most Filipinos are risk averse and lack the time and expertise to invest on their own, they tend to pass the responsibility to another company by purchasing an educational plan or life insurance policy.

Renelyn Arellano, a law student recently got a variable life insurance policy for her one-year old daughter. “When I was offered this product by my financial adviser, I immediately liked it and it was better than the education plan that was earlier offered to me. The returns may not be guaranteed but it certainly have the potential to match the tuition increase.” That is because the policy is linked to the performance of either the bond or equity market. While she is clearly aware of the risks associated, Renelyn is nonetheless willing to take the chance.

By leveraging on these asset classes, an annual investment of P65,000 for the next 16 years at a rate of 8% can help the funds grow to more than P2,000,000. An endowment plan is also a good alternative for those who don’t want to take a risk with variable insurance. But given the benefits it guarantees, an endowment plan naturally comes at a higher premium. A 10-year endowment plan cost more than P1,700,000 but guarantees a fund of P2,100,000in total living benefits that can be use as an education fund when the child starts college six or seven years later.

Whether it is investing on your own or buying a plan, it is important to stay focused on the goal. Jeff recommends a regular rebalancing of portfolio to see whether the investments are doing well or not. That is why there is a need to come up with a basket of three or more investments so that there is a buffer or contingency in case one or two of your instruments are not performing well. Financial advisers have always harped on the benefits of a diversified portfolio. Constantly updating yourself on the current tuition can also help.

Filipino parents’ are notable for sacrificing and saving just to send their children to school and often, at the expense of their own future. It is undeniably a very noble act. Partnering with stable financial institutions and objective financial advisers can make their objective clearer and more achievable. Investing their hard-earned savings using a diversified portfolio of financial instruments – mutual funds, stocks, insurance policies, and endowment plans – can help them realize the ultimate dream of every Filipino parent and save themselves the financial loss, psychological anguish, and emotional heartache suffered by educational plan holders.