10 Money Management Tips For Every Filipino F-R-E-E-L-A-N-C-E-R

By Lianne Martha Laroya

Freelancing is a fulfilling dream – however, this wonderful dream can stop anytime and give you a reality check when you run out of cash and your bills start to pile up. Prevent bankruptcy from happening during your freelance career with these 10 useful money management tips.

A freelancer’s job doesn’t just stop with graphic designing, content writing, data encoding, and program coding. On the contrary, as a freelancer, your marketable skill is the least of your worries! How so? My fellow freelancer, in case you haven’t noticed yet, being a freelancer is different from being an employee. Aside from the fact that you can work in your pajamas at two o’clock in the morning during your work day as a freelancer, you should also realize that in the freelancing world, you are basically left on your own.

So now, you might be asking yourself this question: How can you be able to run your freelance career, develop your freelancing website, get enough paying clients, work on your marketable skill, pay for your monthly bills, promote your freelance services, file your taxes and stay sane enough to enjoy the benefits that freelancing can offer, every month?

It’s fairly simple. You just need to read these 10 beneficial personal finance tips and follow them religiously during your freelancing days.

F – Focus on the Entrepreneurial Mindset

Being a freelancer means that you’re self-employed. Being self-employed means that you’re running your own business. And running your own business means that you should always think of everything you do from an entrepreneur’s standpoint.

Freelancing isn’t just a “raket” – it’s not a hobby that you do in your spare time. It’s your main source of income. It’s what brings in the money. It provides for your needs. It’s supposed to be treated as a full-time business.

Register your freelancing career with BIR – tell them that you’re a self-employed professional and specify the kind of services that you’re offering to your clients. This will get your head in the game and really encourage you to take freelancing seriously. Open a separate bank account for your freelancing business. Do this so that you won’t get your personal and your professional matters mixed together. One of the worst things that you can do is using your marketing budget to pay for your groceries!

R – Review Your Monthly Income Records

One of the disadvantages of freelancing is that you can’t quite pinpoint the exact amount you get per month simply because your income is fluctuating. Last month, you may have been having a feast since you were able to earn P100,000, while this month, no client may be contacting you and thus you’re experiencing famine.

In order to get your average monthly income, take your income these past three months and divide them by three. So if you had P25,000 in January, P23,000 in February, and P40,000 in March, your average monthly income is P29,000. Getting your average monthly income is important because you will be basing your budget (your saving and spending plan) from this figure. You can’t know how to reach a target if you don’t know what the target is!

You can also get your hourly rate by dividing your monthly income with the number of hours you work per month. In the same example, if you work for 120 hours per month, your hourly income is roughly P240/hour. Now, let’s say you want to buy a dress worth P2,400. Would you really want to sacrifice 10 working hours just for one dress?

E – Evaluate Your Savings and Expenses

Right now, can you tell me how much you save per month for your savings and investments?

Do you also know how much money you spend per month?

All these questions can be answered if you take the time to track them either manually or digitally. A classic pen and paper can track them decently, but if you really want to get specific, a spreadsheet on your computer can do the job just fine, too.

If you’re spending your monthly income up to the last centavo, you’re not doing it right. What you should do instead is to save first before spending anything. The easiest formula that you should remember is:

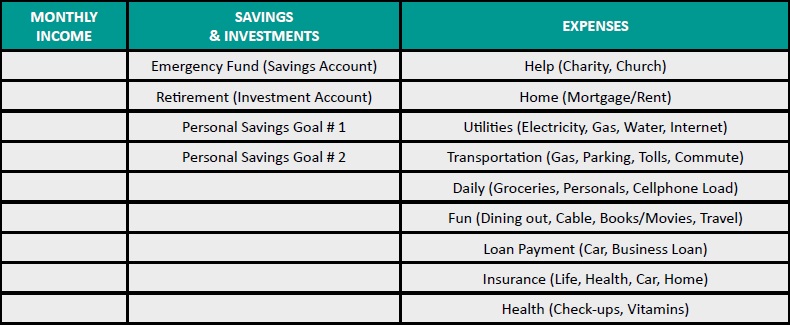

Income – (Savings & Investments) = Expenses

E – Establish Your Emergency Fund First

Your emergency fund is crucial. It’s absolutely required that you save up for this before anything else. As a freelancer, there will be times when your clients may all just decide to disappear on you, your regular client may not have enough money to pay you, or you may be struck by a debilitating illness that may prevent you from working altogether.

Your emergency fund covers you whenever any of these unfortunate incidents occur. A target amount for this would be three to six months’ worth of your monthly expenses. So, if you spend P20,000 monthly, your emergency fund should be P60,000 to P120,000.

In order to keep motivated to work on your savings, you should remember the answers to these questions:

Why are you saving? You need to save because you’re not sure if your income this month will be enough to pay for your needs. You don’t want to drown in debt. And you most certainly don’t want to harass your relatives to lend you money just so you could pay for your electric bill.

Where can you save? Look at your areas of fun – most of the time, that dress, that movie, that dining out, that gadget, and that tea latte can be cut back in order to give you more cash for your savings.

How can you save? Take advantage of automation. Before paying Henry Sy, Jaime Zobel de Ayala or Tony Tan Caktiong, pay yourself first by depositing at least 10% of your salary to your savings account. It’s perfectly fine to start with at least 10% first, because you want to make saving a habit. You want to enjoy saving – think of it as giving your older self a gift!

You worked hard and spent a lot of hours just to be able to earn your monthly income. Don’t you think it’s right that you get to be paid first?

L – Look Out For Delays

Another difference between freelancing and employment is that your income as a freelancer may experience delays. There will be times when your client will prefer to pay you on a twice a week basis while other clients may need to pay you on a monthly basis only. This is problematic since your bills won’t wait for you to have cash – bills will come, whether you’re loaded with money or not.

The key here is to include potential delays in your money management efforts:

a. Bill your clients regularly

Dedicate a special day of the week for billing your clients on a consistent basis. How about billing them every Tuesday and giving them a two-week notice before the payment date?

b. Discuss the possibility of including “payment milestones” in your contracts

You can negotiate with your clients the option of “payment milestones,” especially if you’re going to be working on a big project with them. Instead of getting the full payment after submitting the whole work, why don’t you split the work into four parts and receive payment for every submitted work?

For example, if you’re going to be working on editing a 40,000-word book, suggest submission of the work and receiving of the payment for every edited 10,000 words.

c. Ask for an upfront payment

If you don’t have any previous working experience with your current client, consider asking them for at least 10% upfront payment before you start doing any work.

Get rid of their doubts by presenting them your portfolio, giving them professional references who can vouch for your integrity and updating them regarding the project’s progress regularly. Asking for upfront payments is also a good way of screening bad clients from the good ones.

A – Ask About Health Insurance Policies Relevant to Your Situation

Don’t just be satisfied with the benefits that PhilHealth can offer you because these benefits are only good for hospital confinement. In the event that you get hospitalized and require emergency care, an account with an HMO can be your best bet as they can pay for your outpatient bills for you.

Since getting an individual account is more expensive, why don’t you get your other freelancing friends to form a group with you and avail of the HMO group plans instead? It’s much friendlier to your wallet if you do it this way.

N – Never Be Tempted by the Thought of Lifestyle Inflation

As a freelancer, you might find that you will have less expenses because you don’t need to commute to work anymore, you don’t need to buy work-related wear anymore and you don’t need to eat out for lunch during your work days anymore.

So because of this, you might be left with more money than what you’re used to. Before you even think about using that money to purchase gadgets not related to your freelancer career, stop and think for a while first.

Use your extra money to purchase work-related equipment, save it, invest it, or splurge in experiences with your loved ones instead. More money doesn’t necessarily mean more expenses. Mostly, it can mean more savings and more investments as well.

C – Cash is King

If you know, deep in your heart, that you’ve always had a problem with consumer debt, don’t aggravate the problem by depending on your credit card. Instead, use cash to help you purchase your essentials. Not only will you get higher discounts, you will also get to experience being overly inquisitive. There is just something about handing out your hard-earned cash to the cashier that makes you want to really reconsider if you should make a purchase or not.

You can approach this in two ways – either have P100-bill denominations only so you think you’re spending a lot more, or have P1,000-bill denominations only so you don’t want to see your big bill be broken down into smaller change.

E – Envelope-Based Budgeting is Perfect to Really Make You Think Twice About Spending Your Hard-Earned Cash On Unnecessary Stuff

To really get the feel of budgeting, use real-life envelopes for your budget and use online transfer for your savings.

You tend to underestimate the value of your money when you’re just looking at a bunch of numbers online, so you tend to save more. After all, what’s a few thousand pesos? You can simply transfer it online to your savings account, right?

On the other hand, you tend to overestimate the value of your money when you’re literally touching every peso bill, so you tend to spend less. After transferring your money from your salary account to your savings account online, do this next: get five envelopes and label them with the category of your expenses, such as Help (Charity, Church), Home (Mortgage/Rent), Utilities (Electricity, Gas, Water, Internet), Fun (Dining out, Cable, Books/Movies, Travel) and Daily (Groceries, Personals, Cellphone Load).

Allocate a certain amount for a certain category and do not touch your savings account anymore. You can only cheat with the money that you’ve put in your envelopes. So, if your electric bill is a bit higher than what you expected, you may need to cut back on your dining out in order to find a balance again.

R – Retirement Planning Should Be One of Your Priorities

Voluntary remittance to SSS is a good and basic plan for you. However, don’t think that SSS is your only option for retirement! Investing in mutual funds is a wonderful money-worker for you. Start planning for them by reading up on money management books, browsing through personal finance blogs and attending wealth conferences and money summits.

You might not have a boss because you’re running a freelancing business.

But practicing these 10 money management tips will definitely make you more in control of your freelancing finances. Reporting to no boss, spending more time with your loved ones and still earning money? At the end of the day, this picture displays what a freelancer’s dream is all about.