The Truth About Retirement: What You Need to Know

Retirement is a chapter in life that many look forward to, yet few are truly prepared for. An online survey

Read More

Retirement is a chapter in life that many look forward to, yet few are truly prepared for. An online survey

Read More

Life insurer Pru Life UK is teaming up with CIMB Bank Philippines (CIMB PH) to make digital financial products and

Read More

Are you on the verge of a loan default? Loan payments might not be made on time due to various

Read More

CIMB Bank Philippines said on Thursday that the gross transaction value of its digital transactions in the first nine months

Read More

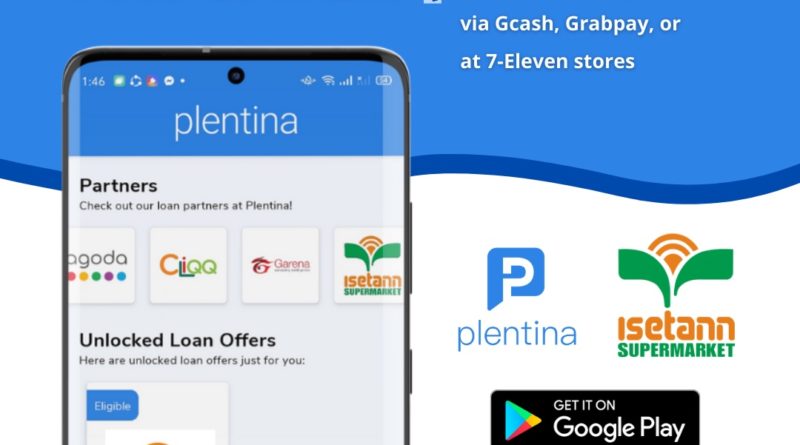

This September, Plentina and Isetann Supermarket teamed up to offer convenient Buy Now Pay Later (BNPL) options for Isetann Supermarket

Read More

Philippine National Bank (PSE: PNB) is launching two new global feeder funds which will allow Filipino investors to further diversify

Read More

Financing company UnaPay, registered in the Philippines under the business name Digido Finance Corp., is helping Filipinos overcome financial challenges

Read More

The Securities and Exchange Commission (SEC) has considered favorably the shelf registration by Jollibee Foods Corporation (JFC) of P20 billion

Read More

Philippine National Bank (PSE: PNB) is offering the Personal Equity and Retirement Account or PERA starting September 2021 through its

Read More

Newly listed Filinvest REIT Corp. (FILRT) declared a cash dividend Tuesday, barely a month since its successful debut on the

Read More

The Securities and Exchange Commission (SEC) has considered favorably the maiden public offerings by Allied Care Experts Medical (ACE) Center-

Read More

The Philippine Digital Asset Exchange (PDAX), the country’s leading cryptocurrency exchange licensed by the Bangko Sentral ng Pilipinas (BSP), has

Read More

The Securities and Exchange Commission (SEC) is paving the way for more innovations in the fintech industry to further promote

Read More

As more consumers shop online for everything, from food delivery to groceries and entertainment, they expect more flexibility, convenience, and

Read More

The Securities and Exchange Commission (SEC) has considered favorably the initial public offering (IPO) of Saint Pio’s Medical Center, Inc.

Read More

Introducing new in-app products and services to make finance easy, approachable, and accessible to all Filipinos! 12 May 2021, Manila,

Read More

The Bank of the Philippine Islands (BPI) offers new digital payment solutions to make everyday banking transactions more convenient for

Read More

BPI Asset Management and Trust Corporation (BPI AMTC), the largest standalone trust corporation in the Philippines, recently launched two new

Read More

BDO Unibank’s foray into sustainable investments continues to pay dividends even amid the pandemic, following the global trend of strong

Read More

BPI Asset Management and Trust Corporation (AMTC), a wholly owned subsidiary of the Bank of the Philippine Islands (BPI), is

Read More