FEdCenter and NDC: A Strategic Synergy Driving Innovation and Financial Inclusion in the Philippines

By Rhea Vitto Tabora The National Development Company (NDC), a state-owned investment firm, has found a strategic ally in The

Read More

By Rhea Vitto Tabora The National Development Company (NDC), a state-owned investment firm, has found a strategic ally in The

Read More

City Savings Bank (CitySavings), the thrift bank subsidiary of the Aboitiz-led Union Bank of the Philippines (UnionBank), makes supporting public

Read More

(L-R) Don Timothy Buhain – Chief Executive Officer, Rex Education, Atty. Dominador Buhain – Chairman, Rex Education, Maye Yao Co

Read More

The Bangko Sentral ng Pilipinas (BSP) advises the public to remain vigilant when receiving Philippine banknotes by carefully checking the

Read More

Bangko Sentral ng Pilipinas (BSP) Governor Benjamin Diokno said that a main lesson from the COVID-19-induced recession is how interlinkages

Read More

Are you on the verge of a loan default? Loan payments might not be made on time due to various

Read More

The Land Bank of the Philippines (LANDBANK) wishes to clarify that the LANDBANK cards being provided for free to unbanked

Read More

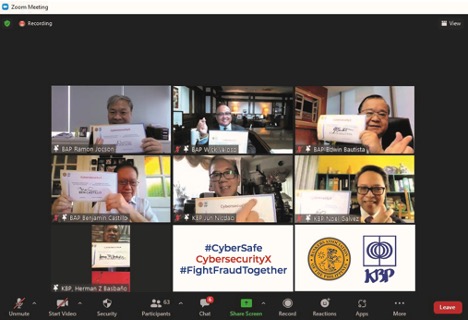

The Bankers Association of the Philippines (BAP) has launched its Anti-Scam Campaign, a wide-ranging information campaign undertaken with various partners

Read More

Five companies building financial technology (fintech) solutions for the Philippine market have shown promising potential after a year of mentorship

Read More

The BSP has constructed the Philippine Financial Social Accounting Matrix for 2017 (PFSAM 2017), which provides an overview of the

Read More

BDO Unibank on Wednesday formally welcomed Hidilyn Diaz, the Philippines’ first-ever Olympic Gold medalist, to its family of brand ambassadors.

Read More

IBM is providing no-cost, online coursework and a digital badge credential in a collaboration with Adobe, the tech giant said

Read More

If there’s a silver lining to the lockdown, it’s that it accelerated the growth of e-commerce in the Philippines. NielsenIQ

Read More

After being lulled into a COVID-19 pandemic stupor the past year, the Philippine stock market is now abuzz with exciting

Read More

The Philippine Stock Exchange, Inc. (PSE) and its partner school De La Salle-College of Saint Benilde, Inc.’s (DLS-CSB) School of

Read More

The Social Security System (SSS) now offers an online learning platform to all members, employers, and other stakeholders to learn

Read MoreIn celebration of its 70th year of delivering service and dedication to Philippine education as a creator and publisher of

Read More

Contract signing for sealing of partnership between Commission on Higher Education (CHED) and REX Education held last January 30, 2021.

Read More

BPI Asset Management and Trust Corporation (AMTC), a wholly owned subsidiary of the Bank of the Philippine Islands (BPI), is

Read More

School Year 2020-2021 has already started, with the so-called “new normal” of education already in place. To cope with the

Read More